Page 171 - Pharmacy Appeals 1/4/04 to 31/3/05

P. 171

NHS Resolution Annual report and accounts 2021/22 147

CNST IBNR: reasonable range

The CNST IBNR provision is the single largest element For this assessment, a number of assumptions are varied

within the total provision. Changes to the assumptions together but the variations are limited to those that could

underpinning this element have the greatest potential have reasonably been chosen based on the same analysis

to affect the estimate of the total provision. of past data. Changes in individual assumptions may have

a greater or smaller impact on the provisions estimate.

The CNST IBNR provision in the accounts is based on a

set of chosen assumptions. It is possible to have a range Although it should be noted that this in itself does not

of different results if a different set of assumptions had reflect the potential uncertainty in the assumptions

been chosen. To illustrate this, a reasonable range is underpinning the provision as future experience may

shown in the following material to demonstrate how differ to the past, changes may occur in the claims

different judgements on the main assumptions, given and legal environment, and the modelling approach

the current environment and the same overall approach, may not be a perfect representation of real life.

could result in different values for the provision.

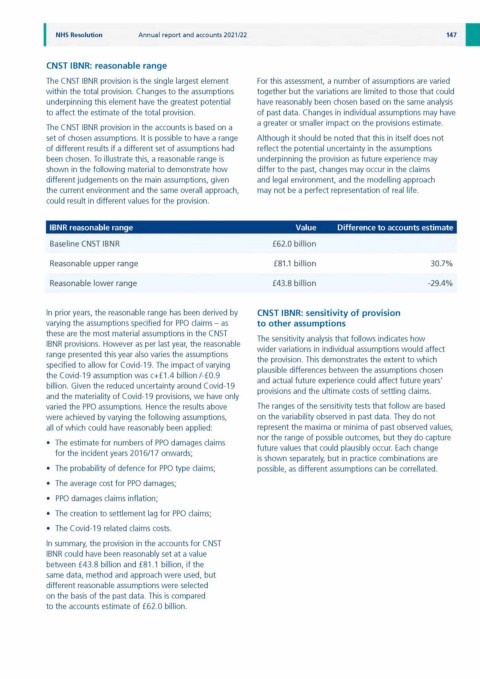

IBNR reasonable range Value Difference to accounts estimate

Baseline CNST IBNR £62.0 billion

Reasonable upper range £81.1 billion 30.7%

Reasonable lower range £43.8 billion -29.4%

In prior years, the reasonable range has been derived by CNST IBNR: sensitivity of provision

varying the assumptions specified for PPO claims - as to other assumptions

these are the most material assumptions in the CNST

The sensitivity analysis that follows indicates how

IBNR provisions. Plowever as per last year, the reasonable

wider variations in individual assumptions would affect

range presented this year also varies the assumptions

the provision. This demonstrates the extent to which

specified to allow for Covid-19. The impact of varying

plausible differences between the assumptions chosen

the Covid-19 assumption was c+£1.4 billion /-£0.9

and actual future experience could affect future years'

billion. Given the reduced uncertainty around Covid-19

provisions and the ultimate costs of settling claims.

and the materiality of Covid-19 provisions, we have only

varied the PPO assumptions. Plence the results above The ranges of the sensitivity tests that follow are based

were achieved by varying the following assumptions, on the variability observed in past data. They do not

all of which could have reasonably been applied: represent the maxima or minima of past observed values,

nor the range of possible outcomes, but they do capture

• The estimate for numbers of PPO damages claims

future values that could plausibly occur. Each change

for the incident years 2016/17 onwards;

is shown separately, but in practice combinations are

• The probability of defence for PPO type claims; possible, as different assumptions can be correllated.

• The average cost for PPO damages;

• PPO damages claims inflation;

• The creation to settlement lag for PPO claims;

• The Covid-19 related claims costs.

In summary, the provision in the accounts for CNST

IBNR could have been reasonably set at a value

between £43.8 billion and £81.1 billion, if the

same data, method and approach were used, but

different reasonable assumptions were selected

on the basis of the past data. This is compared

to the accounts estimate of £62.0 billion.