Page 170 - Pharmacy Appeals 1/4/04 to 31/3/05

P. 170

146 Financial statements

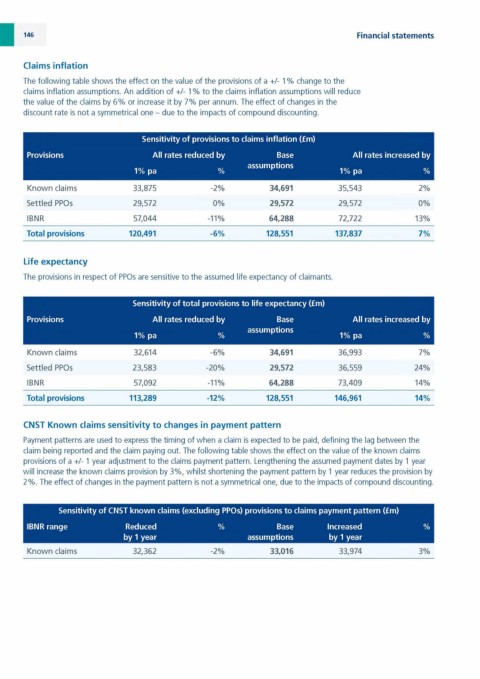

Claims inflation

The following table shows the effect on the value of the provisions of a +/- 1% change to the

claims inflation assumptions. An addition of +/- 1% to the claims inflation assumptions will reduce

the value of the claims by 6% or increase it by 7% per annum. The effect of changes in the

discount rate is not a symmetrical one - due to the impacts of compound discounting.

Sensitivity of provisions to claims inflation (f m)

Provisions All rates reduced by Base All rates increased by

assumptions

1% pa % 1% pa %

Known claims 33,875 -2 % 34,691 35,543 2 %

Settled PPOs 29,572 0 % 29,572 29,572 0 %

IBNR 57,044 -1 1 % 64,288 72,722 13%

Total provisions 120,491 -6% 128,551 137,837 7%

Life expectancy

The provisions in respect of PPOs are sensitive to the assumed life expectancy of claimants.

Sensitivity of total provisions to life expectancy (f m)

Provisions All rates reduced by Base All rates increased by

assumptions

1% pa % 1% pa %

Known claims 32,614 -6 % 34,691 36,993 7%

Settled PPOs 23,583 -2 0 % 29,572 36,559 24%

IBNR 57,092 -1 1 % 64,288 73,409 14%

Total provisions 113,289 -12% 128,551 146,961 14%

CNST Known claims sensitivity to changes in payment pattern

Payment patterns are used to express the timing of when a claim is expected to be paid, defining the lag between the

claim being reported and the claim paying out. The following table shows the effect on the value of the known claims

provisions of a +/- 1 year adjustment to the claims payment pattern. Lengthening the assumed payment dates by 1 year

will increase the known claims provision by 3%, whilst shortening the payment pattern by 1 year reduces the provision by

2%. The effect of changes in the payment pattern is not a symmetrical one, due to the impacts of compound discounting.

Sensitivity of CNST known claims (excluding PPOs) provisions to claims payment pattern (f m)

IBNR range Reduced % Base Increased %

by 1 year assumptions by 1 year

Known claims 32,362 -2 % 33,016 33,974 3%